Skip to the main content.

.svg)

![]()

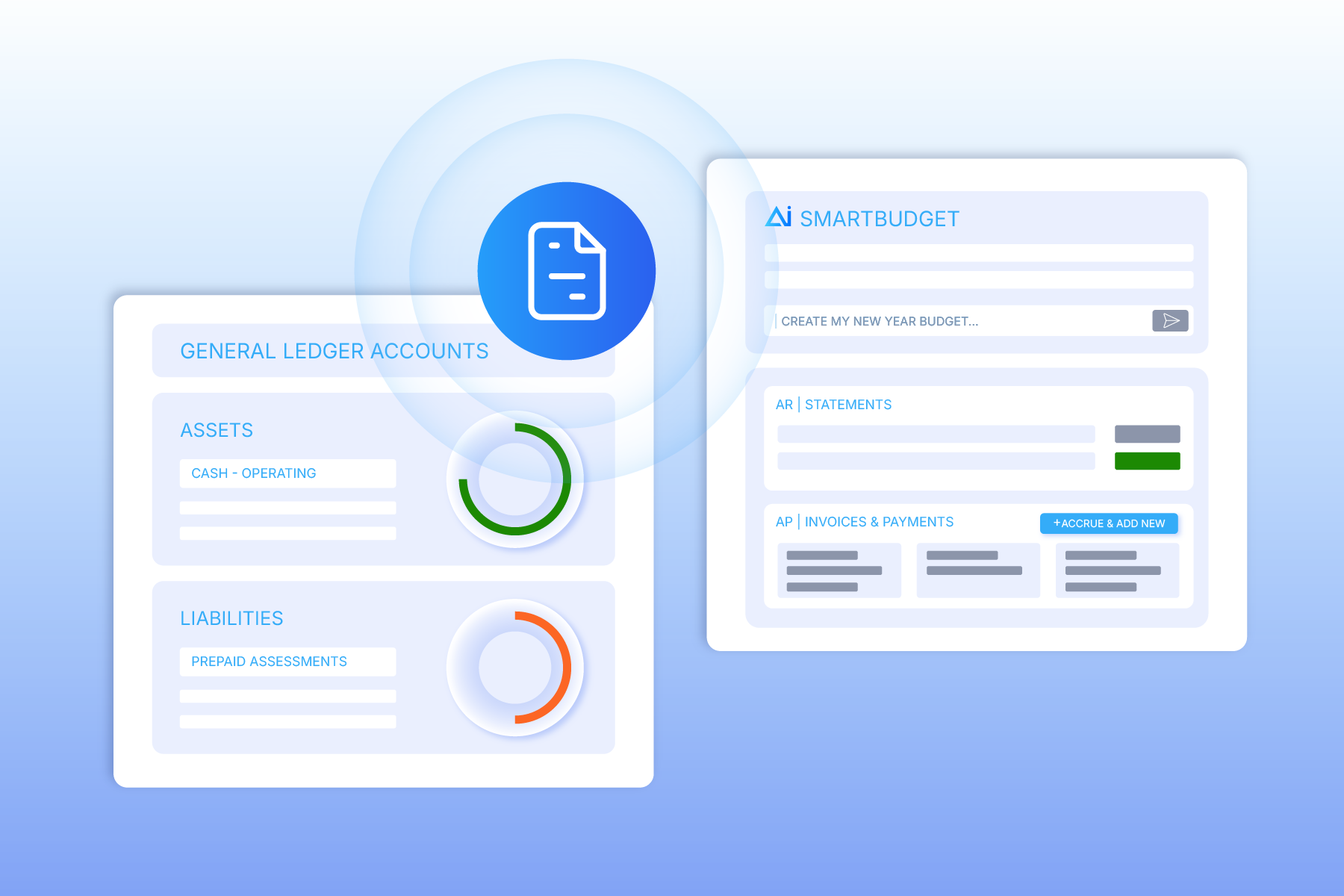

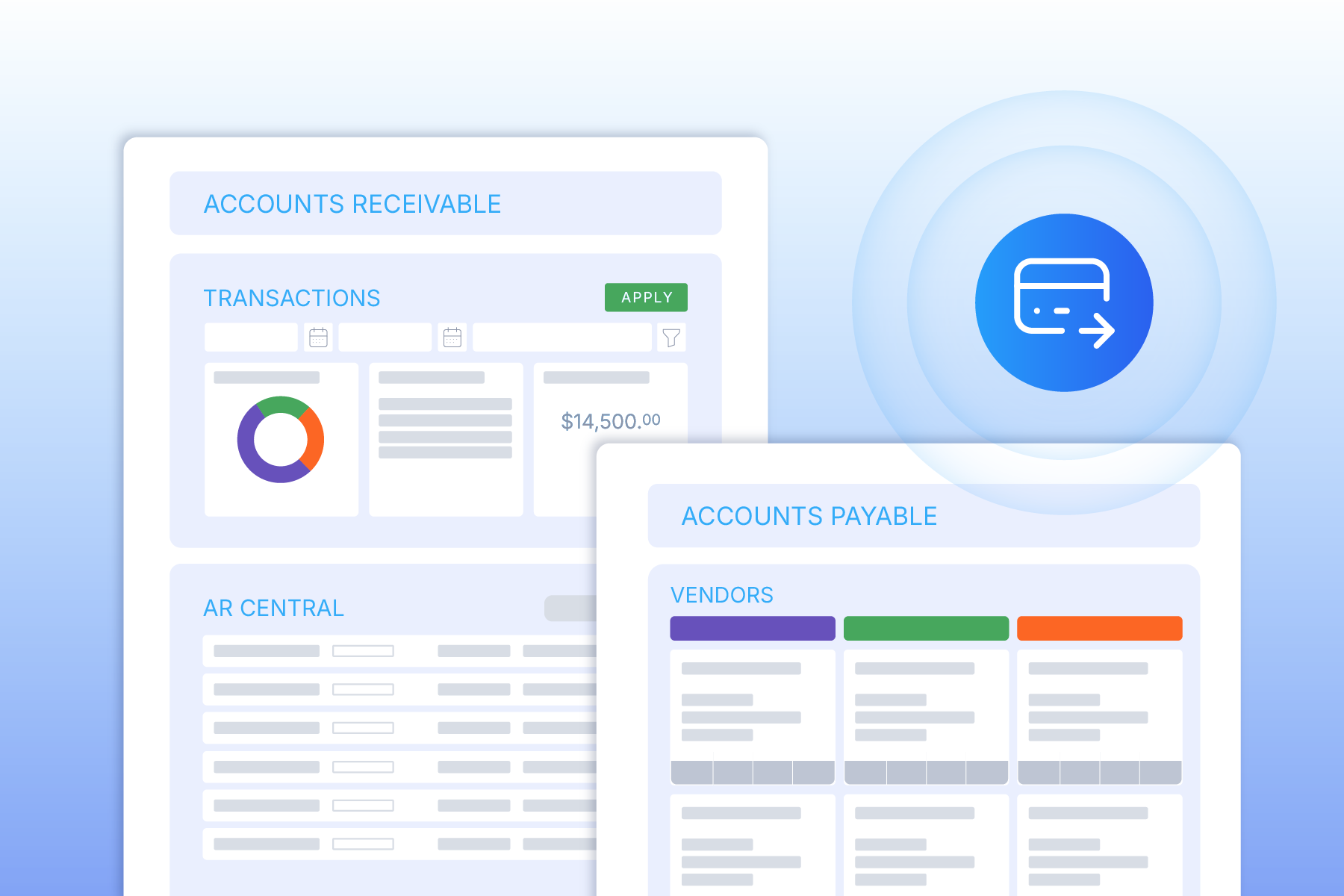

Enumerate Central

Run accounting, payments, and operations in one connected system.

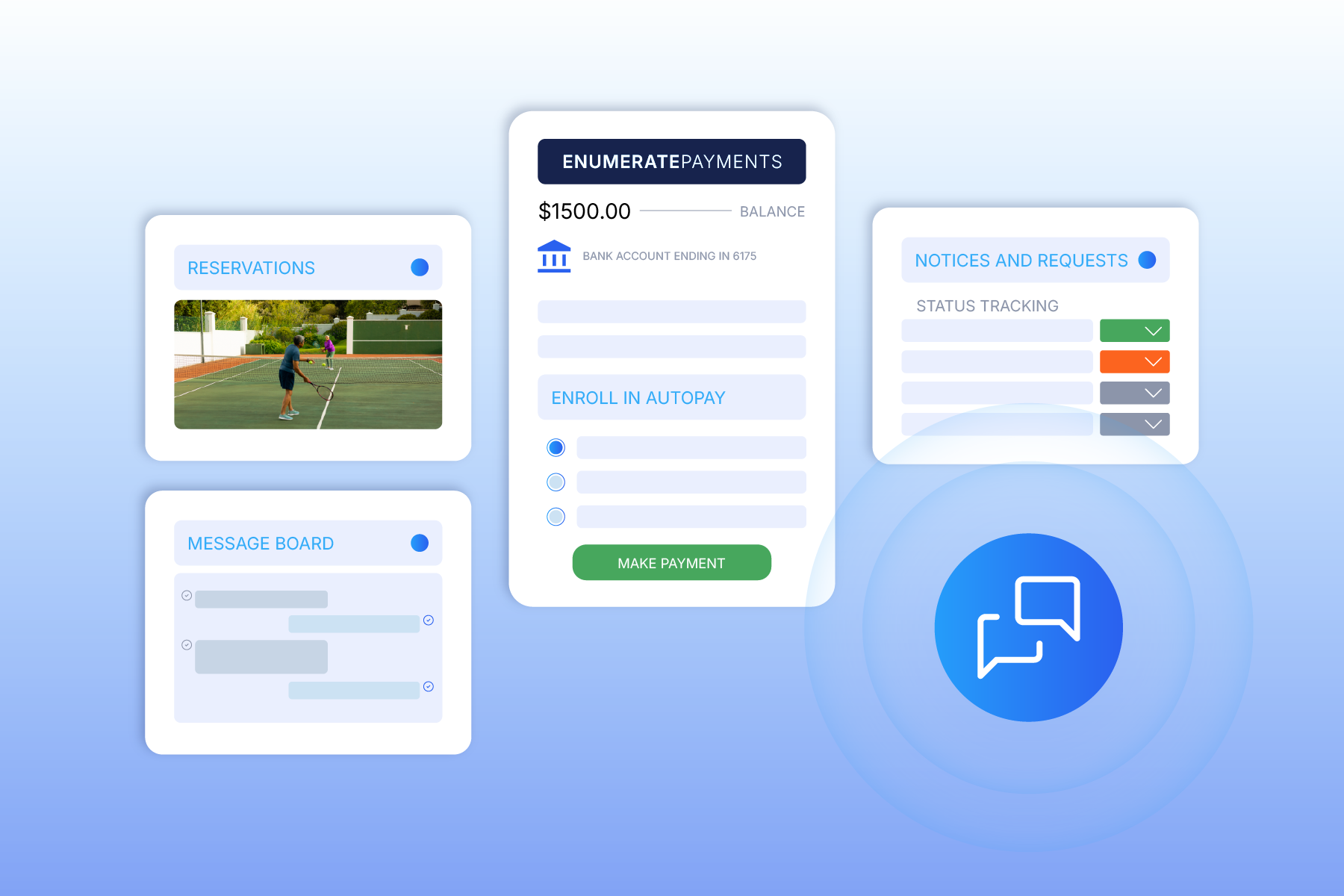

Enumerate Engage

Make it easy for homeowners and boards to pay, communicate, and stay informed.

Numa AI

Automate work and get answers instantly, right inside your workflows.

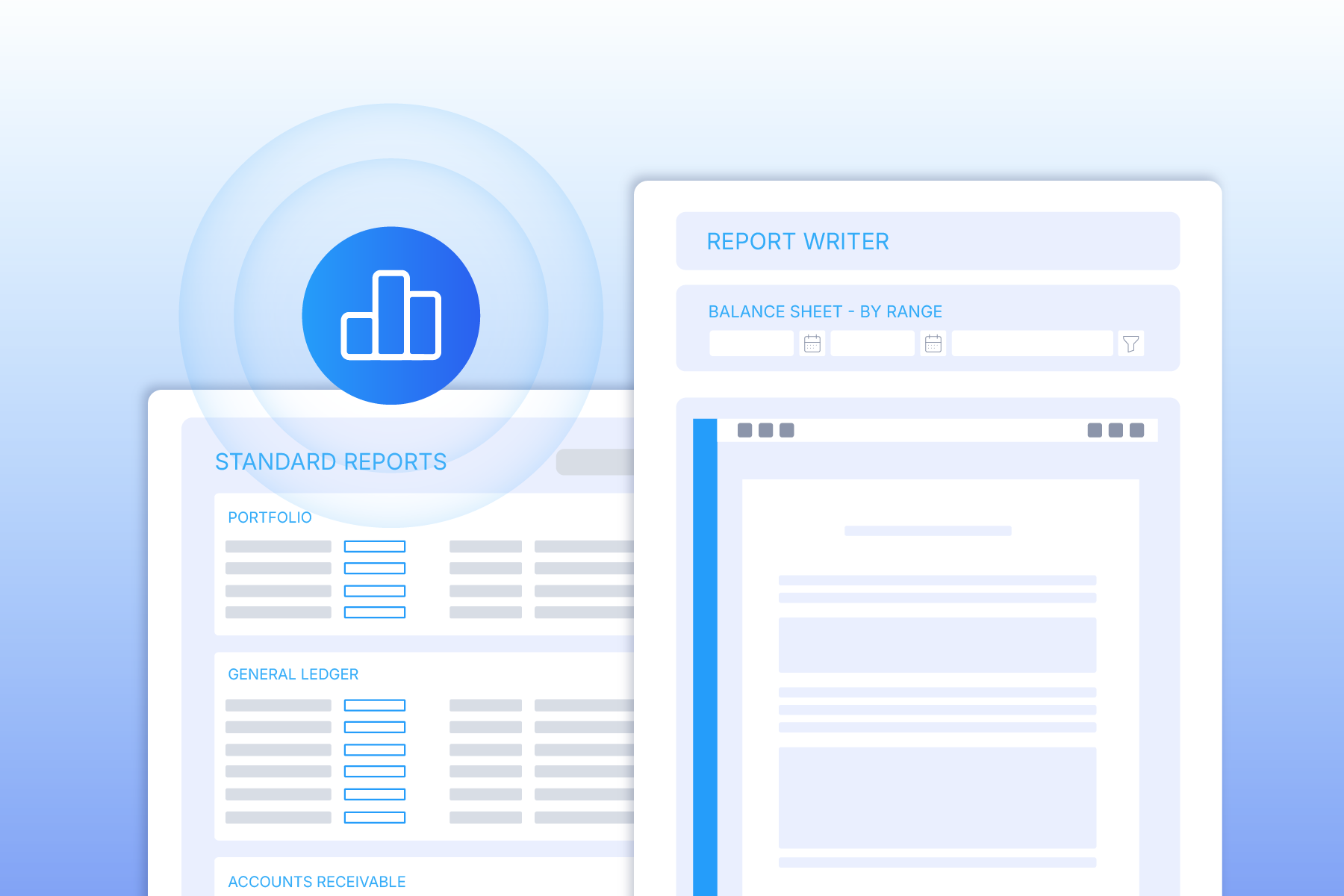

Enumerate Financial Services

Accurate community accounting, handled by experts with built-in controls.

Numa AI

Intelligence, Built In.

Built into the workflows your team already uses to reduce manual work, deliver faster answers, and help your team scale confidently.

Learn more about Numa AI